Though considerable information has been released since the signing of the U.S. tax reform legislation in December 2017, we realize that many individuals are asking the question “how does the new tax law affect me personally?” With 2018 already underway, we wanted to illustrate some of the major ways in which your tax bill and paycheck could change under the new tax structure. This case study blog highlights five categories of individuals to demonstrate the recent changes that we expect will most prominently affect our individual clients, with comparison charts to reflect the changes to expect between 2017 and 2018.

Keep in mind that this does not encompass all potential tax scenarios, as it is simply a snapshot of some common taxpayer profiles. We always recommend that you discuss any concerns or questions related to how this legislation will affect you specifically with your accountant and/or other professional advisors.

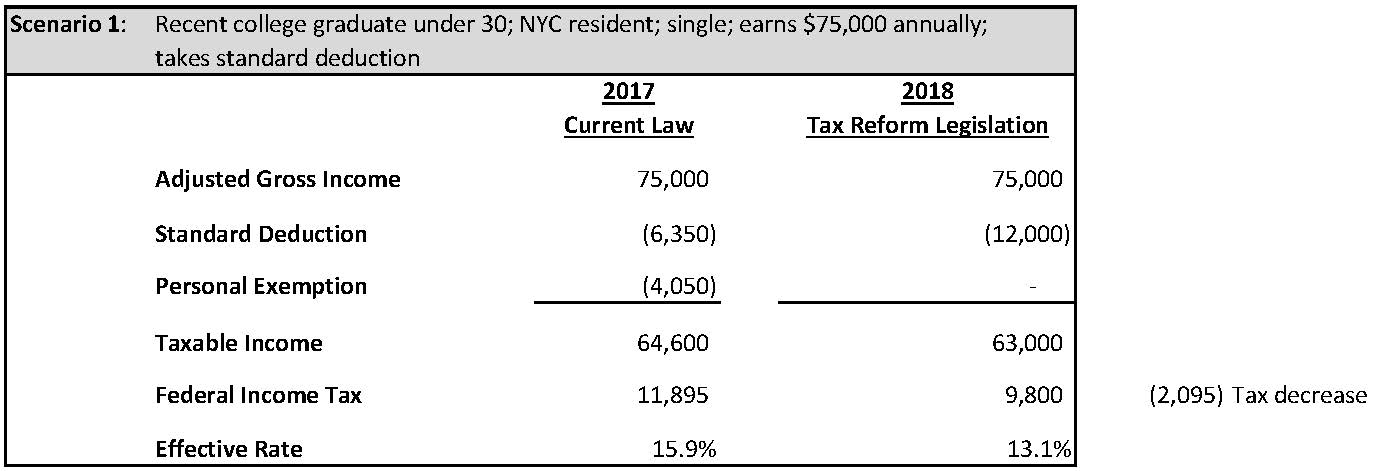

TAXPAYER 1: RECENT COLLEGE GRAD

This individual is a single filer, under 30, earns an annual salary of approximately $75,000, and takes the standard deduction in both tax years (2017 and 2018).

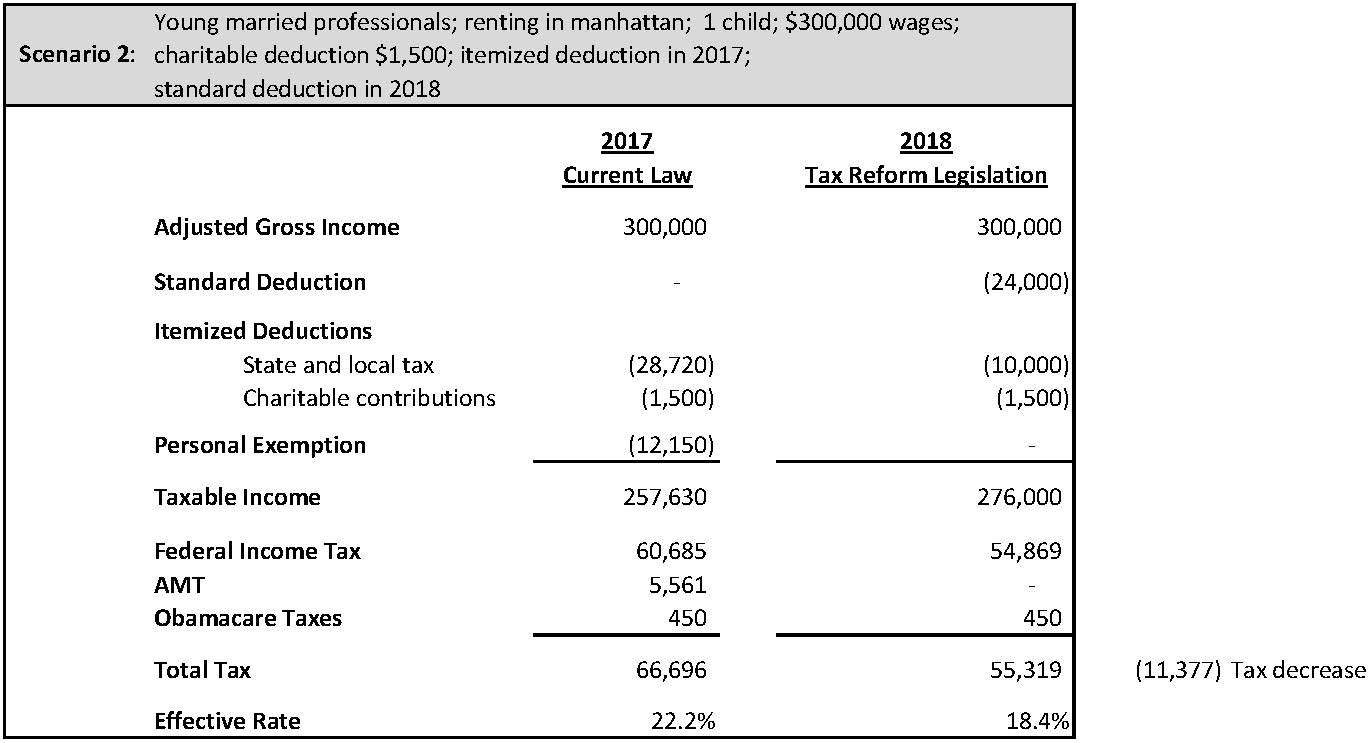

TAXPAYER 2: YOUNG MARRIED PROFESSIONALS

These taxpayers are filing jointly, age 30-40 with one child, renting an apartment in NYC, earning an annual salary of approximately $300,000 and takes a charitable deduction of $1,500.

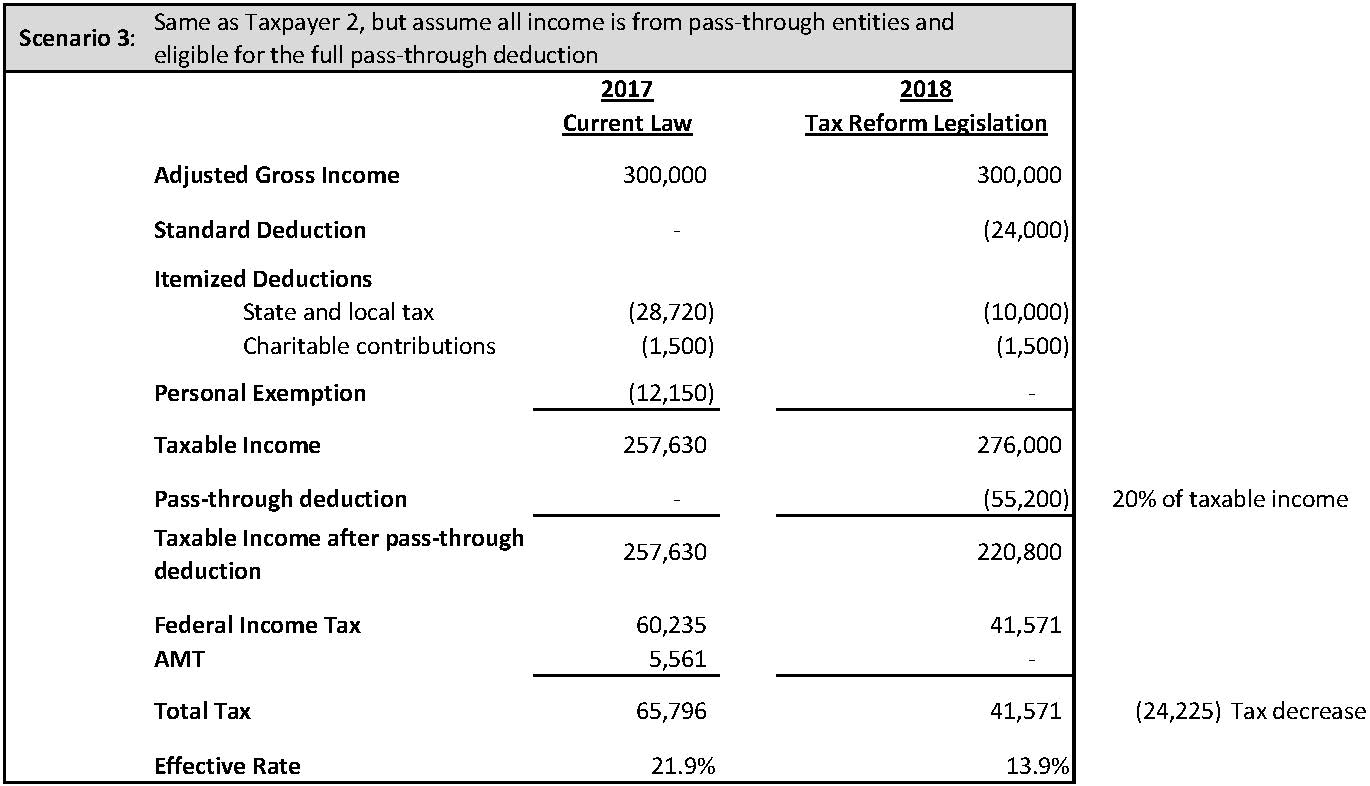

TAXPAYER 3: YOUNG MARRIED PROFESSIONALS WITH QUALIFIED BUSINESS INCOME

This case is similar to Taxpayer 2 (same marital/filing status, one child, renting in NYC, same annual salary), but this taxpayer is eligible for Qualified Business Income from a pass-through entity (this could be an attorney or doctor with an S-Corp).

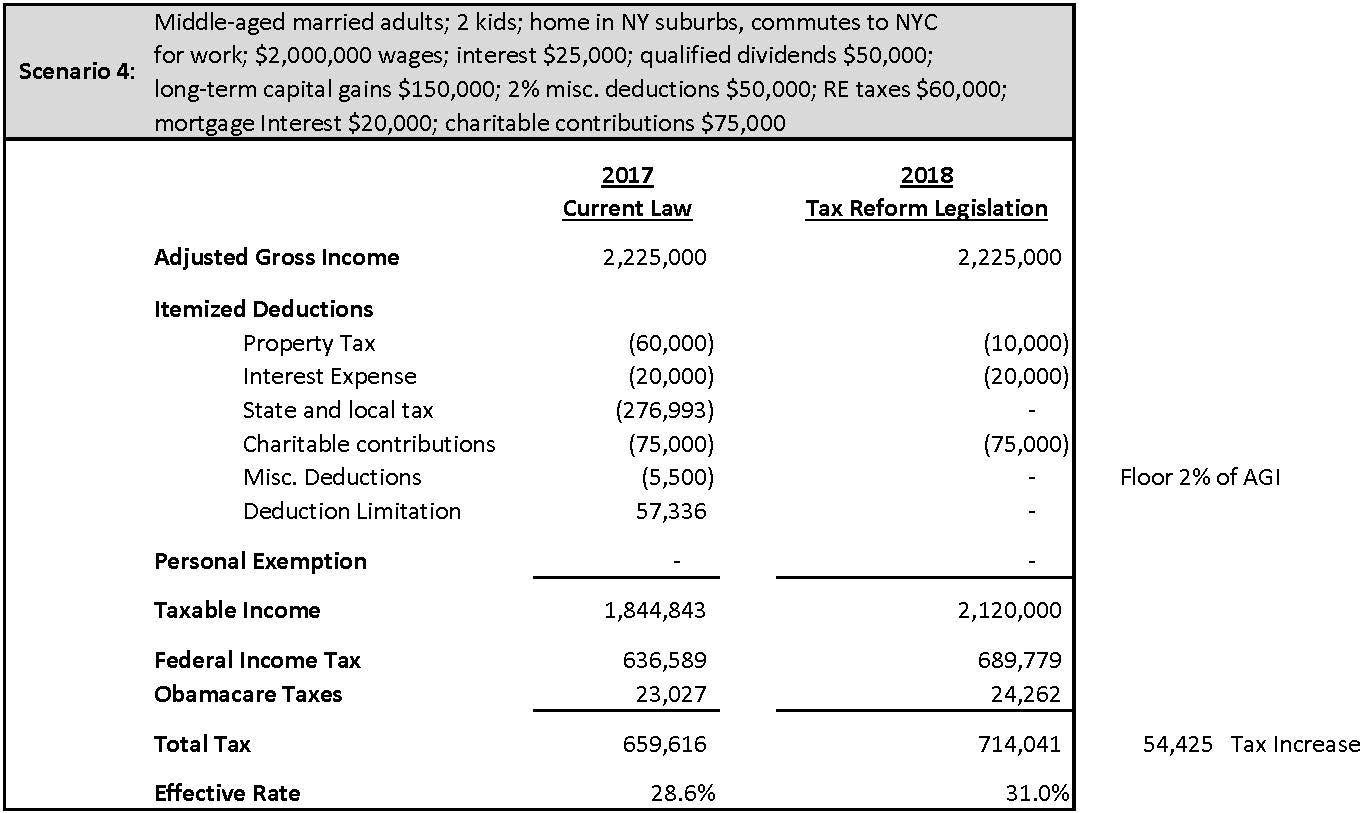

TAXPAYER 4: GEN-X / BABY BOOMER MARRIED PROFESSIONAL

These taxpayers are filing jointly, between ages 50-70 with two children, earning approximately $2,000,000 annually and is a NYS resident commuter. They earn $25,000 in interest, $50,000 in dividends and $150,000 in long-term capital gains. They take a 2% miscellaneous deduction ($50,000), pay $60,000 in property taxes and $20,000 in mortgage interest. Charitable contributions are $75,000.

TAXPAYER 5: RETIRED EXECUTIVE

This individual is married filing jointly, age 70+ with a $300,000 pension, $25,000 in interest, $200,000 in qualified dividends and long-term capital gains of $100,000. They have medical expenses of approximately $100,000, take a 2% miscellaneous deduction ($20,000), pay $60,000 in property taxes and mortgage interest of $20,000. Charitable contributions are $30,000.

ADDITIONAL CONSIDERATIONS

• The new tax law will reduce taxes for many people, especially individuals like Taxpayers 1, 2, 3 and 5 in these case study scenarios, due to the increased standard deduction and the lower tax rates.

• Those receiving qualified business income from pass-through entities will be able to take advantage of the new deduction.

• High income taxpayers who reside in states with high tax rates (i.e. NY, NJ, CT, CA, IL) will see an increase in their taxes. The decreased tax rates are not enough to offset the lost state tax deductions.

• Residents of states with no personal income tax (i.e. FL, NV, TX) should have a substantial tax decrease.

• In 2018, medical expenses and charitable contributions will still be eligible for itemized deductions.

• Substantially fewer individuals will be subject to AMT because the income tax deductions and miscellaneous itemized deduction subject to the 2% AGI floor no longer exist under the new legislation.

FOR MORE INFORMATION

The purpose of this blog is to demonstrate some of the most prominent upcoming changes that can be expected for certain types of individual taxpayers; it should not be referenced as a full guide to the new legislation. We encourage you to contact us with any questions or concerns you may have related to these changes and how they might affect you individually. For such inquiries, or for information about our services, please contact us at info@fffcpas.com or (212) 245-5900.

John Gontijo, CPA, MBA, is a Tax Manager at Farkouh, Furman & Faccio. He has over 10 years of experience with high net worth individuals, small businesses, and international taxation. Prior to joining FF&F, he worked for a niche CPA firm in NYC which specialized in inbound U.S. tax matters for German, Swiss, and Austrian clients, including Offshore Voluntary Disclosure Programs.