On December 22, 2017, President Trump signed tax reform legislation that represents the most significant changes to the Internal Code since 1986. The tax reform bill affects both individual and business taxpayers; below please find a summary of the provisions we expect to most directly affect the majority of our clients. Please note that the legislation is quite complex and that the following summary is merely bullets points of what we feel are the most relevant provisions. Unless otherwise noted, these provisions are effective for tax years beginning after December 31, 2017 (i.e. the 2018 calendar tax year).

SUMMARY OF CHANGES FOR INDIVIDUALS

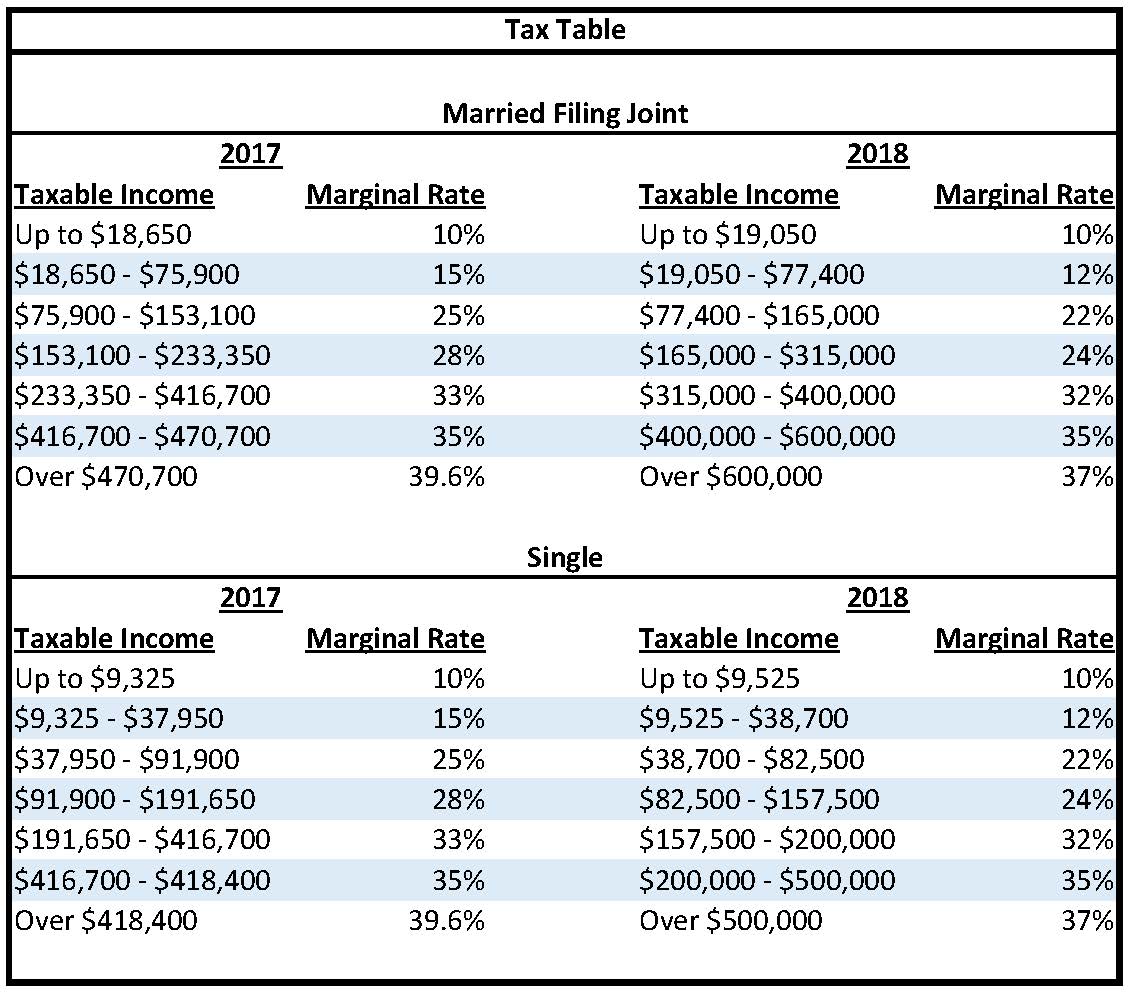

Tax Rates

The bill maintains 7 tax brackets with modified rates. The top individual rate is lowered from 39.6% to 37%, which will apply at taxable income of $500,000 for single taxpayers and $600,000 for taxpayers married filing joint.

Below please find a comparison of the 2017 tax rates to the 2018 rates under the new bill (click to enlarge).

Standard Deduction and Personal Exemption

The $4,050 per person personal exemption, which was previously subject to a phase-out, has been suspended for tax years beginning after December 31, 2017 and before January 1, 2026. To compensate for the loss of the personal and dependent exemption as well as many other popular itemized deductions, the available standard deduction has almost doubled to $12,000 for single filers and $24,000 for spouses filing a joint return for tax years beginning after December 31, 2017 and before January 1, 2026.

Itemized Deductions

Taxpayers may deduct the greater of the standard deduction, or their itemized deductions. The use of certain itemized deductions has been limited for tax years beginning after December 31, 2017 and before January 1, 2026:

– The combined amount of State and local income tax and property tax that may be deducted is limited to $10,000. State and Local taxes paid in 2017 for the 2018 tax year may not be deducted until 2018.

– The deduction for mortgage interest is limited if the amount of the new mortgage indebtedness exceeds $750,000. No deduction will be allowed for interest on home equity indebtedness. The deductibility of home indebtedness interest paid on mortgages existing prior to December 15, 2017 continues to be subject to a limitation on the interest paid on $1 million of outstanding mortgage debt.

– Miscellaneous itemized deductions subject to the 2% floor, such as investment fees and employee trade or business expenses, have been suspended.

– Casualty losses in respect to property are limited to those losses incurred in a federally-declared disaster area.

– In a benefit to taxpayers, the AGI limitation on cash charitable contributions has been increased from 50% to 60%.

– Also a benefit, the floor for deducting medical expenses has been reduced from 10% of AGI to 7.5%.

Alternative Minimum Tax (“AMT”)

Due to an increase in the amount of taxable income which is exempt from the AMT calculation and a significant increase in the income levels ($500,000 single and $1 million married filing joint) at which the exemption will phase out, much fewer individual taxpayers will be subject to the AMT under the new law than are subject to the AMT under current law.

Affordable Care Act Individual Mandate

The shared responsibility payment for failing to obtain health insurance is eliminated beginning after December 31, 2018.

ESTATE AND GIFT

– The Estate tax remains in place.

– The unified estate and gift tax credit exclusion amount is almost doubled to $10 million (adjusted for inflation occurring after 2011) for tax years beginning after December 31, 2017 and before January 1, 2026.

– The Generation-Skipping Transfer Tax (“GST”) exemption is also increased to $10 million.

PASS-THROUGH ENTITIES

Pass-Through Deduction

– For tax years beginning after December 31, 2017 and before January 1, 2026 an individual taxpayer may deduct 20% of qualified income from a partnership, S corporation or sole proprietorship.

- Must be a domestic business to qualify.

- Investment income of a pass-through entity does not qualify.

- S corporation payments deemed to be compensation do not qualify.

– The deduction reduces taxable income, not AGI.

– If taxable income is in excess of a threshold amount, the deduction may not be taken for certain specified service businesses.

- Specified service businesses include performance of services in the fields of law health, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees or owners, or which involves the performance of services that consist of investing, investment management trading, or dealing in securities, partnership interests, or commodities.

– The deduction is limited to half of the wages paid by the pass-through entity (or the sum of a quarter of the wages and a percentage of the cost basis of fixed assets if this computation is more beneficial).

– Trusts and Estates are eligible for the 20% deduction.

Carried Interest

In order for partnerships to pass through long term capital gain income to partners who hold a carried interest, the partnership must have held the asset generating the long term capital gain for more than 3 years prior to its disposition by the partnership.

Losses

The maximum aggregate loss from businesses that may be taken by a non-corporate taxpayer is limited to $250,000 ($500,000 if married filing joint). Excess amounts are carried forward. The limit is applied at the partner or S corporation shareholder level.

Click here for some real-life scenarios illustrating how the new law will affect certain individual taxpayers.

FOR MORE INFORMATION

Please be aware that this is simply an overview of the provisions of the tax reform legislation we feel are of direct concern to our clients, and it should not be referenced as a full guide to the upcoming changes. We encourage you to contact us with any questions or concerns you may have related to these changes and how they might affect you individually. For such inquiries, or for information about our services, please contact us at info@fffcpas.com or (212) 245-5900.